Starbucks’ major Chinese rival Luckin Coffee on Monday filed for an initial public offering with the U.S. Securities and Exchange Commission.

Established less than two years ago, the China-based private coffee chain plans to go public on Nasdaq this year under the ticker LK, while showing no sign of turning losses into profits anytime soon.

Luckin’s placeholder value is set at $100 million for its first public offering. It may raise up to $800 million, according to Reuter’s citing sources.. Credit Suisse, Morgan Stanley, CICC (China International Capital Corporation), and Haitong International will participate in underwriting the IPO.

Here’s a brief financial situation of Luckin Coffee from the form F-1:

In 2018, Luckin gained a total net revenue of $1.25 billion but is at a net loss of $2.4 billion. In 2019, for the three months ended March 31st, there was a $710 million net revenue, and an operating loss of $780 million. The net loss attributable to the company's ordinary shareholders and angel shareholders was $85 million in the first quarter of 2019.

Luckin Coffee has become another technology-driven offline service company seeking U.S. public listing while carrying a huge net loss, following Uber.

Its mad offline store expansion is what led it into such a great loss. In twelve months’ time from March 31st 2018 to March 31st 2019, from 290 stores to 2370 stores, the coffee chain scale has reached a growth rate of 700%+.

The total stores now consist of 2163 pick-up stores, 109 relax stores with dine-in features, and 98 delivery kitchens with basically no storefront.

Store rental and other operating costs contributes to the highest operating expenses, followed by costs of materials, general and administrative expenses, sales and marketing expenses and depreciation expenses (in ranking order).

The maddest expansion occurred during the fourth quarter of 2018, when Luckin’s store number grew from 1189 to 2073, with a net increase of 74.3%. During the same period, the operating expenses reached a high of $1.65 billion while recording a net loss of nearly $1 billion.

This does not paint a good picture on the future of the Chinese coffee chain.

Firstly, it’s clear that Luckin’s net revenue growth started to decline:

- 2018 Q1:$1.9 million

- 2018 Q2:$18.7 million(+838%)

- 2018 Q3:$35.8 million(+98%)

- 2018 Q4:$69.2 million(+93%)

- 2019 Q1:$71.1 million(+2.8%)

Secondly, the asset-liability ratio shows no sign of decreasing:

- As of 2019 Q1, Luckin’s assets reduced to $432 million, with a debt of $161 million, an asset-liability ratio at 37.26%.

- As of 2018 Q4, Luckin had $519 million in assets, and $169 million in debt respectively, with an asset-liability ratio of 32.56%.

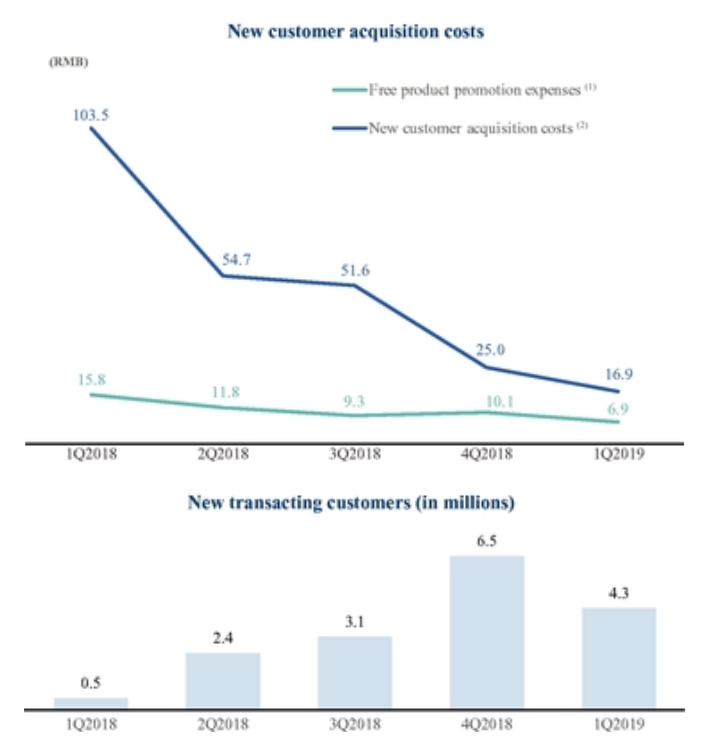

Thirdly, new transacting customers have seen steep decrease in the first quarter of 2019

New customer acquisition costs decreased from RMB103.5 in the first quarter of 2018 to RMB16.9 in the first quarter of 2019 per new transacting customer. The figure shows that the number of new transacting customers drops when the user acquisition costs are reduced.

Finally, the company’s operating cash flow is miserable:

- After cash through financing rounds, the company spent $930 million in the first quarter of 2019.

- $191 million of net cash used in operating activities in order to support massive expansion in 2018.

To sum up, if Luckin Coffee fails to go public in Nasdaq this time, the company’s ability to settle its debt will be significantly reduced, while facing an increased difficulty in business growth.

In the meantime, the Chinese coffee chain is now falling into a business dilemma: while reducing new customer acquisition costs is a feasible way to minimize loss, a result of a slower growth in new customers would makes it even harder to pay off its debts.